In brief:

- A new framework concerning segregated fund guarantee (SFG) risk under OSFI’s life insurance capital adequacy test (LICAT) became effective January 1, 2025, which will improve risk sensitivity and align with other LICAT risk components for other product lines.

- The increasingly complex stochastic calculation under different stress scenarios requires insurers to consider enhancing model capabilities through model transformation with advanced computing technologies.

- Given the wider risk spectrum under the updated SFG risk, insurers will need to reassess and refine their business strategies and product designs.

1. Introduction

OSFI’s life insurance capital adequacy test (LICAT) assesses an insurer’s capital adequacy using a risk-based approach. Until recently, capital requirements for segregated fund guarantee (SFG) risk, a LICAT risk component, relied on calculations established in the early 2000s. Effective January 1, 2025, the calculation was revised to enhance the risk sensitivity of segregated funds and ensure consistency with other LICAT risk components implemented for other product lines.

2. Summary of updates and implications

a. Use of risk-based approach is computationally more intensive

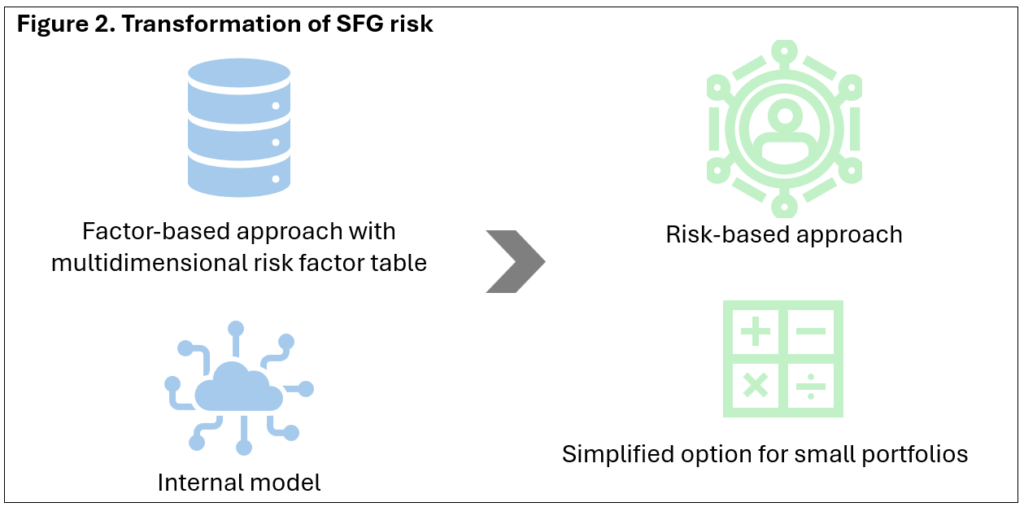

Previously, SFG risk was inherited from minimum continuing capital and surplus requirements (MCCSR) and calculated using a factor-based approach based on product features, policyholder details and fund information, or using OSFI-approved internal models with real-world measures. Effective 2025, SFG risk is calculated by shocking various assumptions similar to other product lines. Given that SFGs are typically modelled stochastically, insurers will need to modify their models to calculate stochastic liabilities under a risk-neutral measure for each stress scenario, unless the SFG portfolios are small enough for a simplified option under the new framework. This would significantly increase operational burden when meeting tight reporting timelines.

Several vendors offer solutions to model SFG and speed up reporting process using advanced computing technologies with distributed cloud processing. Insurers looking to stay ahead of technological trends and enhance model capabilities should consider transforming their models to reduce runtime and increase model efficiency.

b. The consideration of a wider risk spectrum affects business strategies and decisions

The previous approach calculated SFG risk as a total gross calculated requirement with either risk factors or OSFI-approved internal models. The risk factors were comprised of large multidimensional tables, which are difficult to determine which risk attributes contribute to SFG risk, whereas an internal model focused on scenario-tested factors that are typically market-risk-related.

The new approach aligns with other product lines and quantifies the capital requirement from a broader range of risk scenarios, including credit, market, insurance and operational risks. It also incorporates several variations to recognize the characteristics of segregated funds:

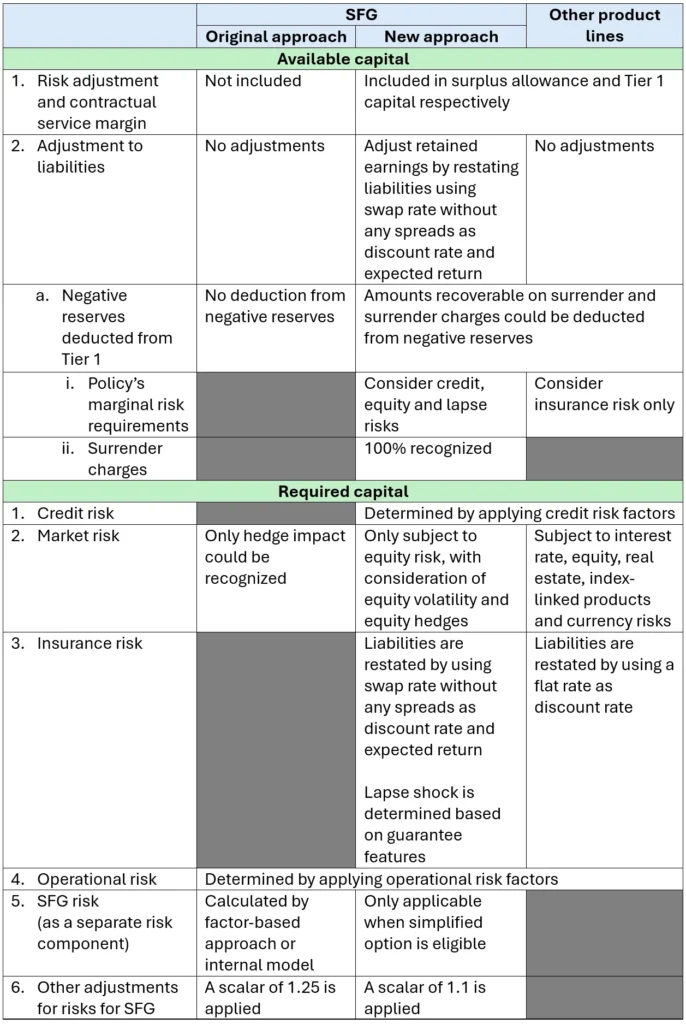

- For available capital (numerator of LICAT ratios), the liabilities from SFGs are restated by using swap rates without any spreads as the discount rate and expected return. This restatement would adjust retained earnings from available capital, and the restated liabilities would serve as the basis for calculating the capital requirement.

- For capital requirement (denominator of LICAT ratios), SFGs are only subject to equity risk under market risk, and it would shock equity value and equity volatility simultaneously with recognition of equity hedges. In addition, for lapse risk under insurance risk, shocks would vary based on the presence of guaranteed withdrawal benefit, dynamic lapse modelling and withdrawal timing.

By considering a wider spectrum of risk, insurers could discover potential vulnerabilities and, hence, refine their capital management strategies (e.g., hedging programs) to mitigate stress impacts and optimize capital. Insurers could also re-examine the pricing metrics of each segregated fund product under the new SFG risk framework and refine product design to maintain profitability.

c. A simplified option is available to reduce capital volatility but confined to small SFG portfolios

Insurers may elect to use the simplified option, which applies a factor to the total guaranteed value based on the type of guarantee, but it is only available when the total guaranteed value does not exceed $100 million. As a result, insurers with small SFG portfolios would not impose a significant operational burden. In addition, from our observation of the market, the SFG risk under this option would result in lower capital volatility. However, insurers need to be prepared to adopt the risk-based approach if adverse economic condition or rapid portfolio growth cause the total guaranteed value to exceed the $100 million threshold.

Table 1. Summary of changes of SFG risk, comparison with other product lines

d. SFG risk is integrated into the risk-based capital framework rather than recognized as a separate item; overall, the change will not cause undue impact with transition measures

Overall, SFG risk is calculated as distinct from other LICAT risk components. Under the new methodology, risks arising from segregated funds are integrated into those risk components. This allows insurers to recognize diversification benefits with different product lines.

To mitigate the effects arising from the effective methodological change, OSFI introduced a scalar applied to SFG risk. In addition, the impact on available capital and capital requirement from the previous three quarters can be averaged to smoothen the impact. Therefore, the new methodology will not cause excessive volatility to the base solvency buffer and LICAT ratios.

3. Conclusion

The LICAT 2025 update shifts SFG risk from a factor-based or internal-model approach to a risk-based one with a simplified option. It enables full integration of SFG risk into the risk-based capital framework, but it also creates implications from operational to risk management perspectives. Insurers need to reassess and refine their reporting models, business strategies and product designs to comply with the new LICAT guideline.

This article reflects the opinion of the authors and does not represent an official statement of the CIA.